Local law 97

Local Law 97 (LL97) is a critical environmental regulation enacted in New York City aimed at combating climate change by reducing greenhouse gas emissions from large buildings. It sets stringent annual carbon emissions limits for buildings over 25,000 square feet and mandates reporting of energy usage and emissions. Building owners must take measures to improve energy efficiency and meet these limits, making LL97 a key component of the city’s sustainability efforts.

Navigating Compliance Excellence

Discover unparalleled Local Law 97 services tailored to propel your building towards emissions compliance and sustainability goals. Our specialized expertise in emissions calculations, reporting, and strategic consulting ensures your property is prepared for a low-carbon future. Partner with us to champion environmental responsibility while achieving regulatory success.

Local Law 97 Compliance Pathways:

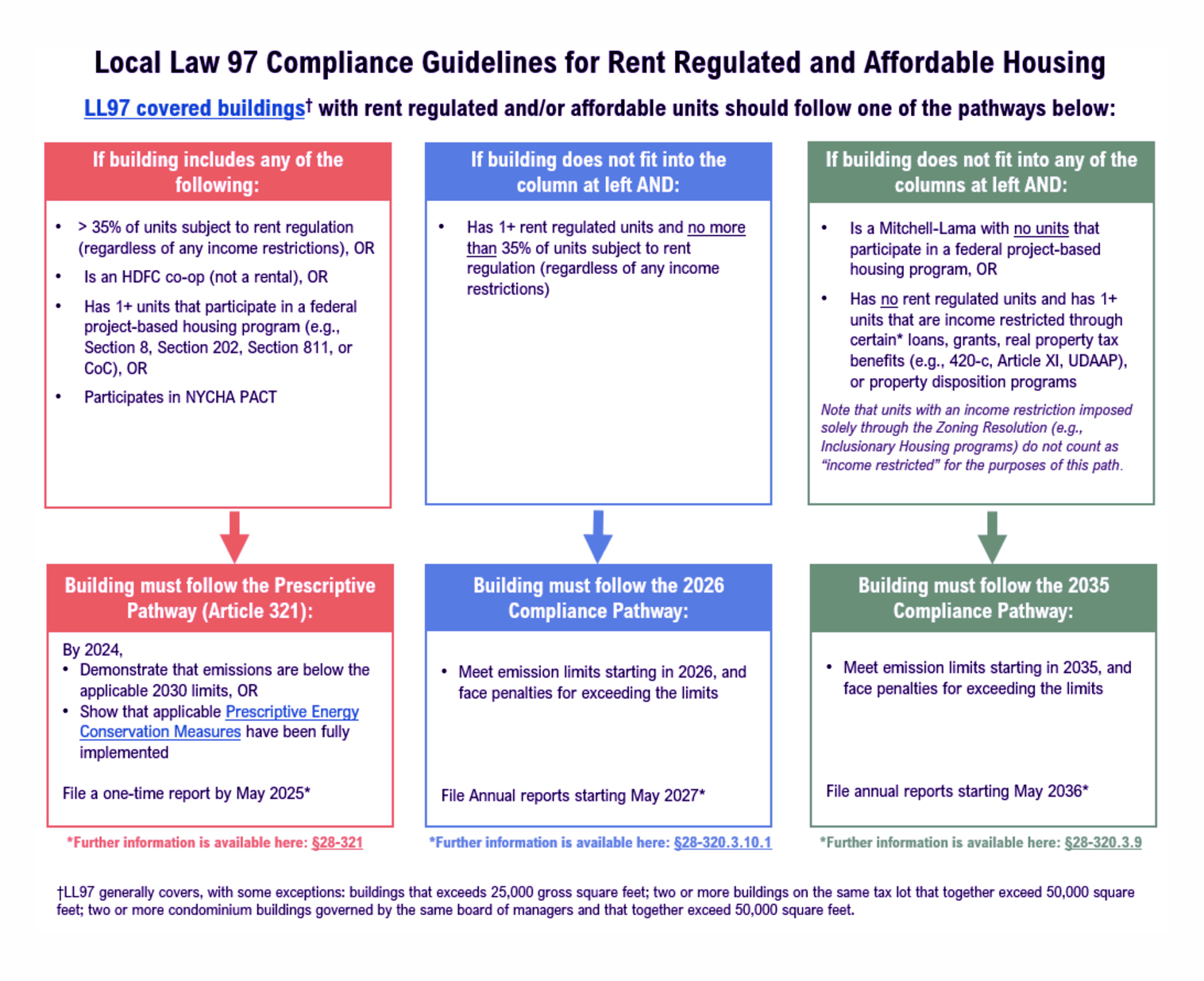

The Standard Pathway mandated by Local Law 97 sets carbon emissions limits for individual properties, necessitating annual demonstrations of emissions falling below these thresholds. Infractions exceeding the limit incur penalties, with a fine of $268 per ton of CO2e. Initially, only 25% of buildings are subject to fines, a figure that escalates to 75% by 2030. Over time, emissions limits tighten progressively, targeting zero emissions by 2050. The baseline year is 2024, with annual reporting obligations commencing from May 2025.

Type of covered buildings:

Article 320 / 1 RCNY §103-14, Building Energy and Emissions Limits:

– Single building > 25,000 GSF;

– Multiple buildings, either on the same tax lot or governed by the same condo board, which are in aggregate > 50,000 GSF (even if individual buildings are < 25,000 GSF).

Not covered until 2026:

– Buildings with at least one, but no more than 35%, rent-regulated dwelling units.

Article 321 / 1 RCNY §103-17, Energy Conservation Measure Requirements for Certain Buildings:

Buildings meeting the same size thresholds as Article 320 that:

– Are mainly used as the assembly space for a house of worship;

– Are certain categories of affordable housing

Under the Prescriptive Pathway, two options exist:

Pathway 1:

installing 13 prescribed measures by December 31, 2024, or reducing emissions below the 2030 limit by the same deadline, both necessitating no further actions in the future.

Pathway 2:

2026 Pathway: mirrors the Standard Pathway but grants buildings an additional two years before enforcement begins, with the baseline year set at 2026.

2035 Pathway: aligns with the Standard Pathway but extends the compliance commencement by 10 years, with the baseline year designated as 2035.

Local Law 97 (LL97),

enacted in New York City, is a groundbreaking environmental regulation designed to address climate change and significantly reduce greenhouse gas emissions associated with the city’s building sector.

Emissions Reduction:

LL97 sets stringent annual carbon emissions limits for buildings larger than 25,000 square feet. These limits are customized based on building type and occupancy, with the goal of substantially reducing emissions over time.

Reporting and Compliance:

Building owners are required to annually report their energy usage and carbon emissions to city authorities. Failure to meet the prescribed emissions limits can result in substantial financial penalties.

Offset Mechanisms:

LL97 offers building owners options for offsetting emissions, including the purchase of Renewable Energy Credits (RECs) or implementing approved emissions reduction measures.

Energy Efficiency Upgrades:

To achieve compliance, building owners may need to invest in energy-efficient retrofits and upgrades to building systems, such as heating, cooling, insulation, and lighting.

Phased Implementation:

The law is implemented in phases, with different emissions limits and reporting requirements for various building sizes and types. Compliance deadlines are staggered to allow for planning and execution.

Environmental Impact:

LL97 aligns with New York City’s commitment to reducing carbon emissions, combating climate change, and enhancing sustainability. The law recognizes the significant role that buildings play in the city’s overall greenhouse gas emissions profile.

Policy Innovation:

Local Law 97 represents an innovative approach to climate action by targeting emissions from buildings, a major contributor to urban carbon footprints, and serving as a model for other cities seeking to address similar challenges.

In summary,

Local Law 97 is a pioneering environmental policy that aims to make New York City’s building stock more energy-efficient, environmentally sustainable, and resilient to the impacts of climate change, while contributing to global efforts to reduce carbon emissions and combat the climate crisis.

FAQs

What is Local Law 97, and what are its goals?

Local Law 97 (LL97) aims to reduce greenhouse gas emissions by 40% by 2030 and 80% by 2050 for buildings over 25,000 square feet.

What are the emissions limits under LL97?

Emissions are measured in tCO2e/sf, with limits varying by building occupancy type for compliance periods (2024–2029, 2030–2034).

What is the prescriptive measures pathway for LL97 compliance?

Certain buildings can implement 13 energy conservation measures (e.g., pipe insulation, radiant barriers) by December 31, 2024, to comply.

What are the penalties for LL97 non-compliance?

Fines are based on excess emissions, calculated at $268 per metric ton of CO2e over the limit, potentially reaching thousands annually.

Which buildings are exempt from LL97?

Exemptions include industrial facilities, low-rise detached buildings, and certain affordable housing with implemented prescriptive measures.

How can owners prepare for LL97 compliance?

Conduct energy audits, review LL84 benchmarking data, and implement measures like efficient HVAC systems and lighting upgrades.

What role does the NYC Accelerator program play in LL97?

It provides free technical assistance and access to incentives for energy efficiency upgrades to meet LL97 requirements.

Can LL97 compliance lead to financial incentives?

Yes, upgrades may qualify for rebates, grants, or tax incentives, reducing costs and improving ROI.

How is LL97 compliance verified?

Owners submit annual emissions reports to the DOB, supported by utility data and proof of implemented measures.

What are the long-term benefits of LL97 compliance?

Reduced energy costs, enhanced building sustainability, and alignment with NYC’s carbon neutrality goals by 2050.

Contact

info@chaptergreencompliance.com

Phone

516-865-4550